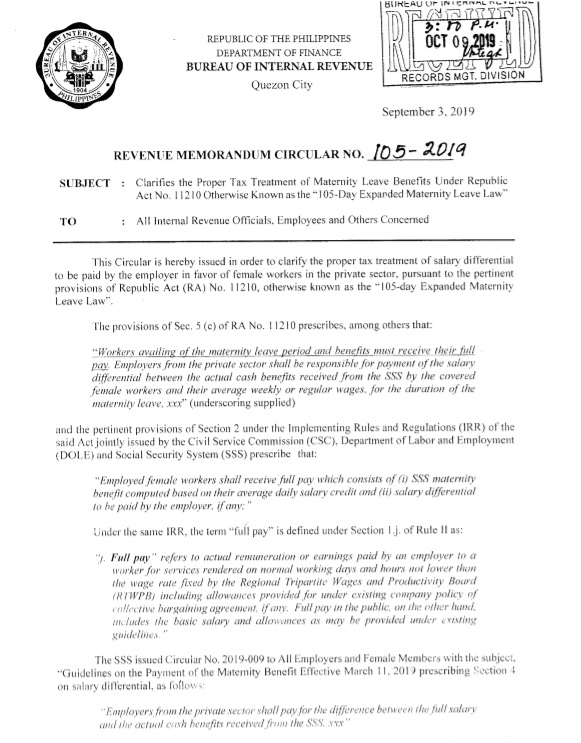

Good news for the workforce, differential from maternity leave benefit is tax-exempt. IRR for tax treatment of the extended maternity benefit was released by BIR last Oct. 9, 2019. The IRR covers the taxability of salary differential from longer maternity leave for the workforce in the private sector.

BIR commissioner Ceasar Dulay said in the memorandum RMC No. 105 – 2019 that “It is clear that salary differential is considered a benefit”. Commissioner Dulay cited Republic Act No. 11210, or the 105 Day Expanded Maternity Leave Act, implementing rules from the act jointly issued by the Civil Service Commission (CSC), Department of Labor and Employment (DOLE), and Social Security Systems (SSS).

As prescribed, “Employed female workers shall receive full pay which consists of (i) SSS Maternity Benefit computed on their average daily salary credit and (ii) salary differential to be paid by employer, if any.”

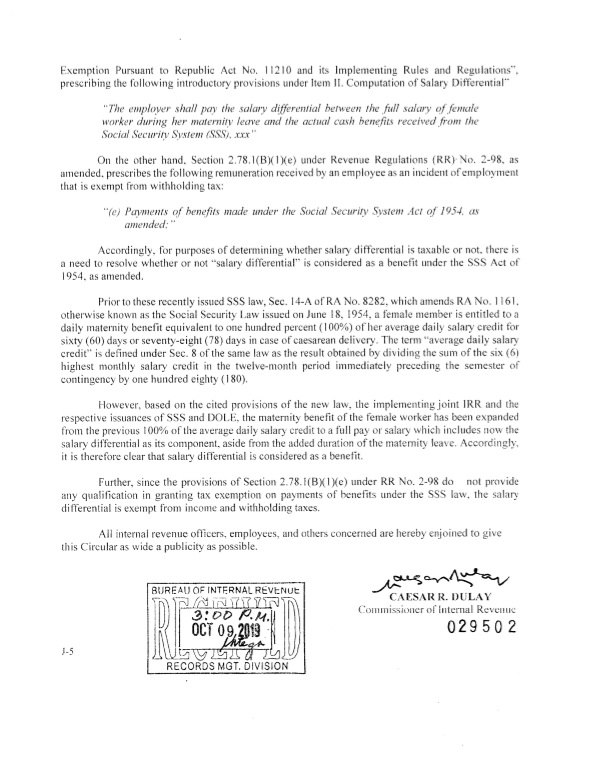

Full payment to employees based on 105 maternity leave is exempt from income and withholding taxes as stated in the memorandum.